Select:

CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS AND FULL YEAR ENDED 31 DECEMBER 2025

Condensed Interim Consolidated Financial Statements for the Six Months and Full Year Ended 31 December 2025

Condensed Interim Consolidated Statement of Profit or Loss and Other Comprehensive Income

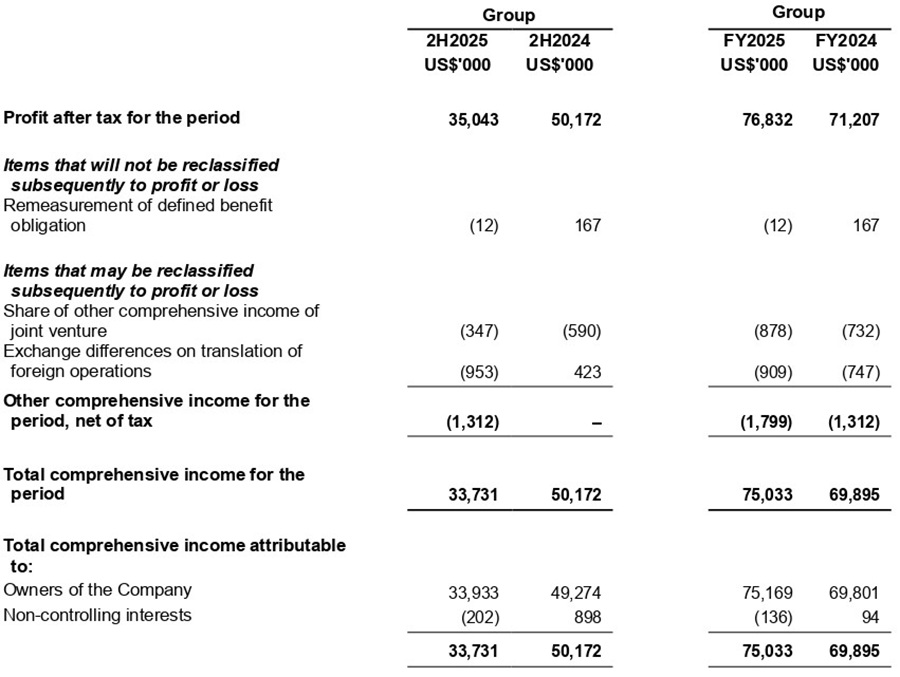

Other Comprehensive Income

Review of Performance

Income Statement

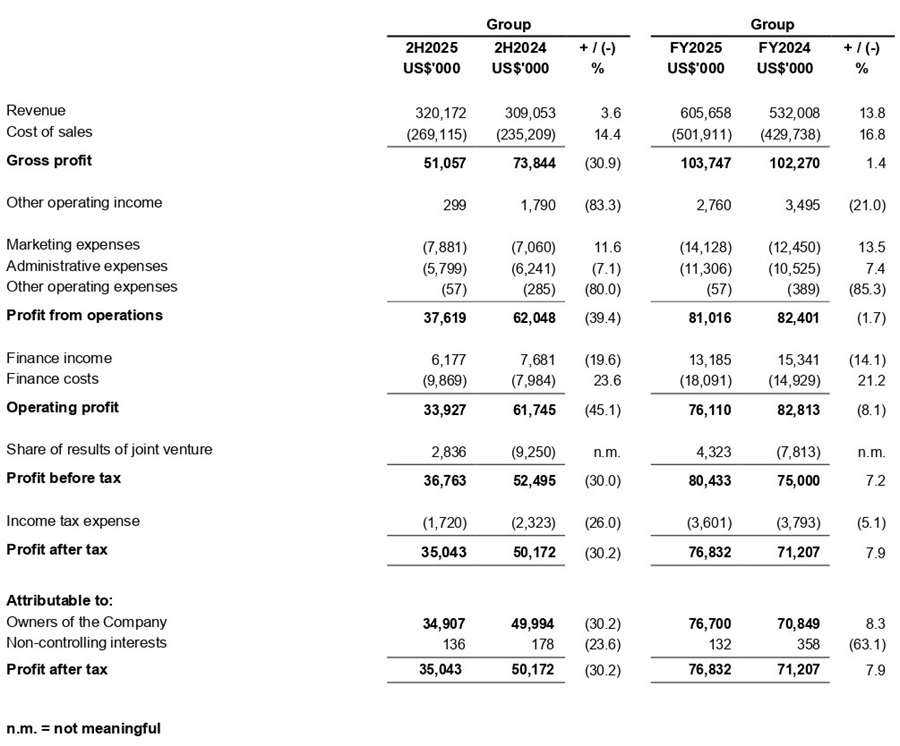

The Group’s FY2025 revenue rose 13.8% to USD605.7 million, from USD532 million in FY2024. For 2H2025, Group

revenue increased by 3.6% to USD320.2 million, compared to USD309.1 million in 2H2024. The improvement in

both periods was driven by higher revenue contributions from all its business segments.

For the Container segment, FY2025 revenue rose 13.6% to USD556.2 million, from USD489.6 million in FY2024.

This took into account a 7.9% increase in container volume handled to 2,062,000 TEUs in FY2025, from 1,911,000

TEUs in FY2024, following the introduction of new services in the Far East, the Indian Subcontinent and the

Philippines, and additional calls deployed on certain routes to meet customer demand. It also factored in higher

average freight rates, as well as selective chartering-out arrangements where certain vessels are deployed to third

parties on temporary basis, as part of the Group’s fleet optimisation strategy.

In 2H2025, Container segment revenue increased marginally by 2.5% to USD294.4 million, from USD287.1 million

in 2H2024. This was mainly due to the additional revenue from chartering activities and a marginal increase in

container volume handled in 2H2025 to 1,073,000 TEUs (2H2024: 1,032,000 TEUs), offset by lower average freight

rates year-on-year.

The Bulk & Tanker segment registered an 18.4% increase in revenue to USD30.9 million in FY2025, from USD26.1

million in FY2024. Revenue for 2H2025 also rose 21.6% to USD16.3 million, compared to USD13.4 million in

2H2024. The increase in both periods was primarily due to higher employment days of vessels.

The Logistics segment delivered a 13.5% increase in revenue to USD18.5 million in FY2025, from USD16.3 million

in FY2024. 2H2025 revenue rose 11.8% to USD9.5 million, from USD8.5 million in 2H2024. The improvement in

the segment’s performance was driven by increase in third-party and fourth-party logistics activities in Indonesia,

as well as new fourth-party logistics contracts secured.

Cost of services increased 16.8% to USD501.9 million in FY2025 (FY2024: USD429.7 million), and 14.4% to

USD269.1 million in 2H2025 (2H2024: USD235.2 million). The increase was broadly in tandem with the increase in

business activity, while factoring in higher charter-hire costs for a larger fleet of container vessels, and higher

amortisation of docking costs as several vessels underwent docking during the year, and higher maintenance and

repair cost in relation to the two ethylene gas carriers.

Taking above into the consideration, gross profit increased marginally 1.4% to USD103.7 million in FY2025, from

USD102.3 million in FY2024. Gross profit for 2H2025 was USD51.1 million, compared to USD73.8 million in 2H2024.

The Group recorded a higher foreign exchange gain of USD1.3 million in FY2025 on the back of stronger Singapore

Dollar against the US Dollar, primarily driven by our Singapore Dollar cash balances.

Other operating income declined 21% to USD2.7 million in FY2025, from USD3.5 million in FY2024, mainly due to

lower gains from the disposal of aged containers.

Finance expenses rose 21.2% to USD18.1 million in FY2025, from USD14.9 million in FY2024. This was mainly

due to higher interest expenses from additional borrowings undertaken in FY2024 for vessel acquisitions, with the

full-year interest impact recognised in FY2025, and increased interest on lease liabilities associated with right-ofuse

assets.

The Group recorded share of profit of USD4.3 million from its joint venture, compared to a share of loss of USD7.8

million in FY2024 due to the absence of impairment losses incurred in FY2024.

The Group posted net profit of USD76.7 million in FY2025, an 8.3% increase from USD70.8 million in FY2024.

Balance Sheet

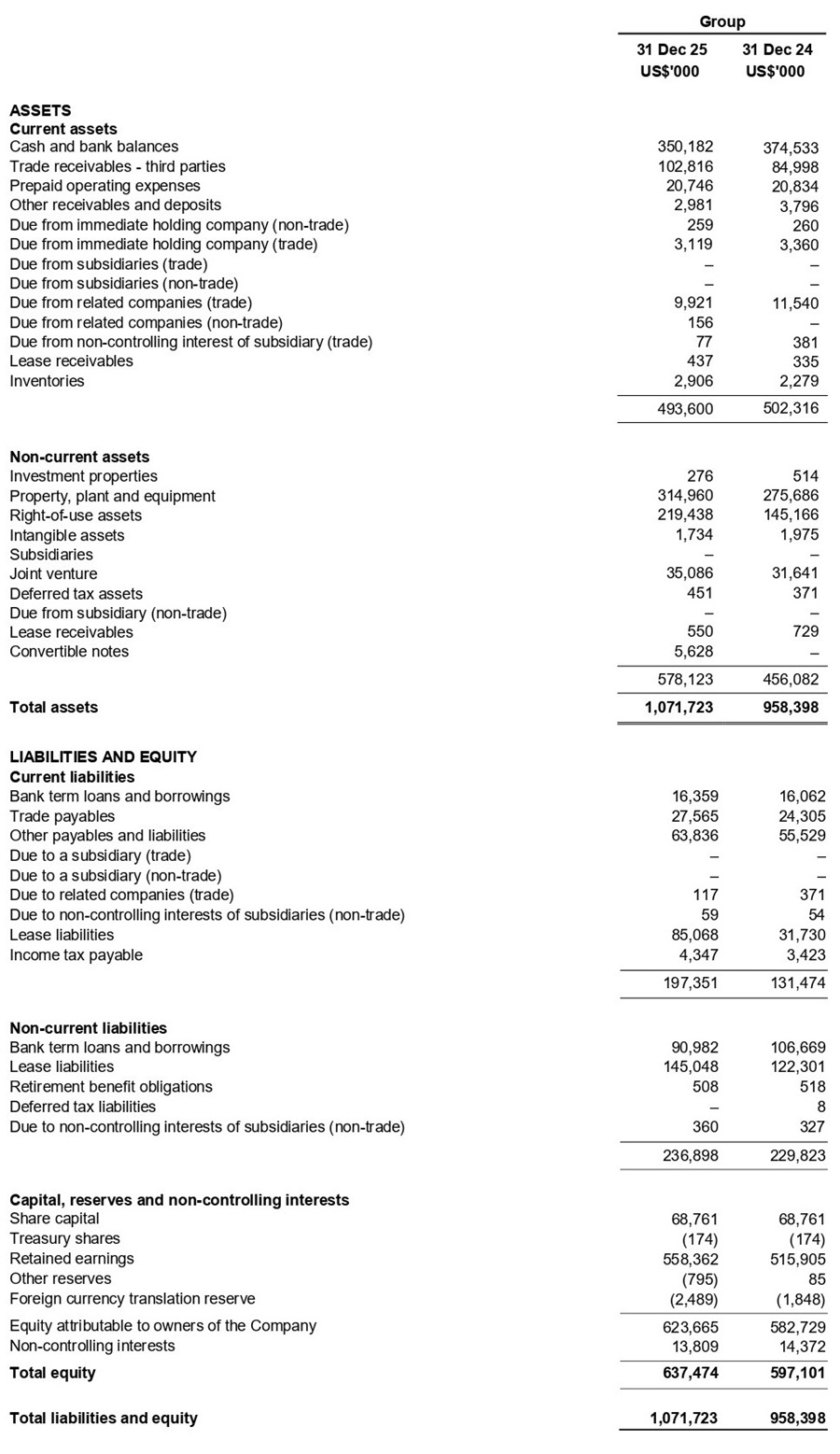

Property, plant and equipment stood at USD315 million as at 31 December 2025, compared to USD275.7 million

as at 31 December 2024. The increase mainly follows the addition of a container vessel into the Group’s fleet in

September 2025. Right-of-use assets amounted to USD219.4 million as at 31 December 2025, compared to

USD145.2 million as at 31 December 2024, largely due to the recognition of right-of-use assets for eight container

vessels following new charter arrangements and lease extensions.

The Group held cash and bank balances of USD350.2 million as at 31 December 2025, versus USD374.5 million

as at 31 December 2024, following the use of funds for the acquisition of a container vessel and an investment in

convertible notes.

Trade receivables and trade payables were higher as at 31 December 2025, compared to 31 December 2024, in

line with the increase in business activity in FY2025.

The increase in current and non-current lease liabilities as at 31 December 2025 is due to the extension of charter commitments for container vessels.

Condensed Interim Statements of Financial Position

Commentary On Next 12 Months Prospects

Amid evolving global trade patterns, geopolitical developments and a complex supply-demand environment, the

Group expects uncertainties in the container shipping market to persist into 2026.

Container freight rates have moderated from previously elevated levels and are expected to remain volatile, with

downward pressure potentially arising from the impact of US trade tariffs and ongoing geopolitical tensions. Vessel

charter rates are also expected to remain relatively firm due to the limited newbuild additions in 2026. In this

environment, the Group believes its fleet profile, disciplined fleet management strategy and focus on service

reliability will position it to navigate the prevailing market conditions.

For the Bulk & Tanker segment, the Group expects operational reliability and performance of its gas tankers to

stabilise, following the completion of technical rectification works. The vessels remain fully employed, and the Group

will continue to focus on improving technical efficiency.

The Logistics segment is expected to continue contributing positively, supported by demand for system-driven

fourth-party logistics solutions. The Group will pursue growth through a combination of organic expansion and

selective investments that enhance service integration and value creation across its supply chain.

The Group sees longer-term growth opportunities across Asia and selected international markets. It will evaluate these opportunities in a measured and prudent manner, with a focus on disciplined capital allocation. The Group is committed to maintain operational resilience and financial flexibility to respond to market developments while pursuing sustainable growth.